Colonial Joins Brookfield’s Growing Pipeline Portfolio in $9B Deal

Plus: We argue that data centers are a bubble and outline portco M&A and exits from last week.

Fall in line.

Last week, Brookfield Infrastructure Partners agreed to acquire Colonial Enterprises, the operator of the largest fuel pipeline (5,500 miles) in the United States.

The $9 billion deal will see Brookfield buy out existing shareholders for a 100 percent stake: KKR (23.4 percent), CDPQ (16.5 percent), IFM Investors (15.8 percent), Koch Inc. (28.1 percent), and Shell’s midstream operating unit (16.125 percent).

The deal is expected to close in Q4 2025 and will be financed with debt led by Morgan Stanley and Mizuho Bank.

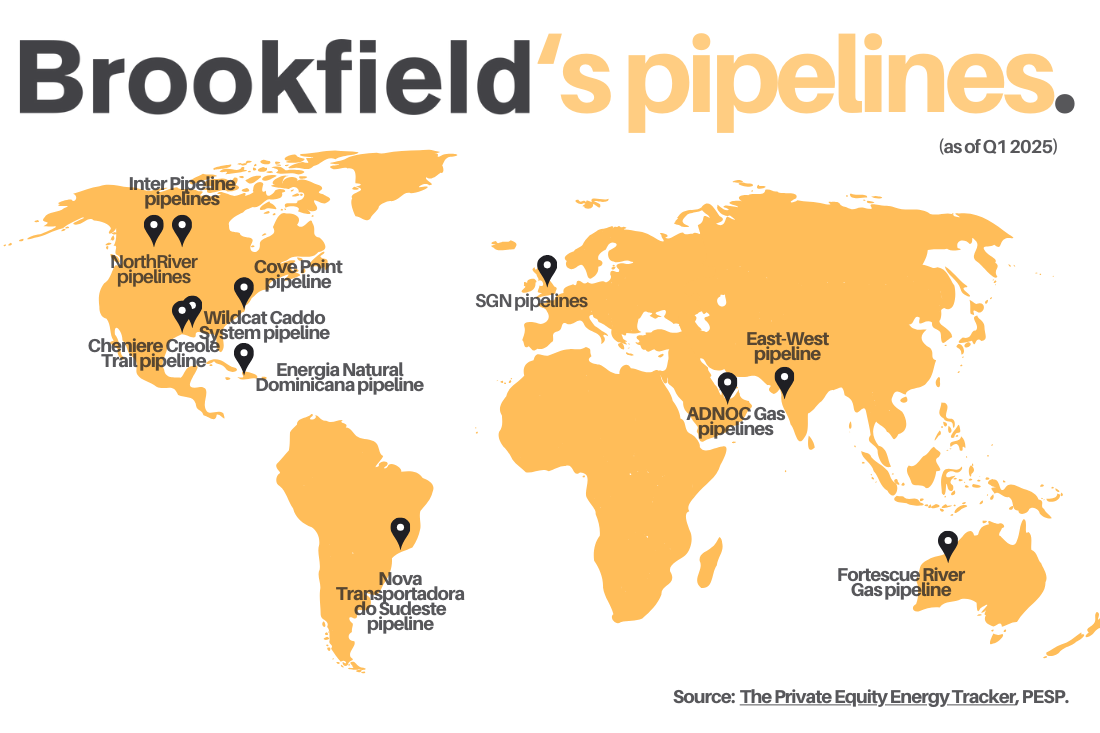

This isn't the first pipeline Brookfield has operated — the asset manager currently owns dozens of pipelines across five continents.

Miles-long history.

Just as Brookfield took on its Colonial pipeline stake, it divested from another large American pipeline operator: Natural Gas Pipelines of America. Its stewardship of the asset gives important context as to how Brookfield operates pipelines in the USA.

On February 15, 2008, Kinder Morgan sold an 80 percent stake in NGPL to Myria Holdings — an investor consortium formed by Brookfield, SteelRiver Infrastructure Partners, PSP Investment Board, and PGGM — for approximately $5.9 billion.

In 2015, Brookfield bought out its Myria partners, paying $106 million to increase its ownership stake from about 27 percent to 50 percent. Kinder Morgan paid $136 million, increasing its ownership from 20 percent to 50 percent, implying a $3.4 billion enterprise value including debt.

In 2021, Kinder Morgan and Brookfield sold a 25 percent stake in NGPL to ArcLight Capital Partners for $830 million, valuing the company at $5.2 billion and bringing Brookfield’s equity stake to 37.5 percent. In 2023, Brookfield offloaded another 12.5 percent to ArcLight.

Finally, Brookfield sold its remaining 25 percent stake to ArcLight last month. The sale generated total proceeds of over $1.7 billion, yielding an 18 percent internal rate of return and a 3x multiple of capital on the investment since the recapitalization in 2015.

Fueling up.

Brookfield’s main method of value creation for NGPL PipeCo was via liquidation of assets. When Brookfield bought its initial stake in 2009, NGPL PipeCo owned 37,000 miles of pipeline infrastructure. By 2015, it had 9,200 miles. And by the time of last month’s divestment, it had only 9,100.

This may prove to be difficult to replicate with Colonial Enterprises. Midstream dealmaking hit a decade low in 2024 despite a global recovery in M&A more broadly.

The incoming Trump administration, though, could change this. The President has voiced support for projects such as the Keystone XL oil pipeline and the Constitution gas pipeline, for example.

A return of a friendlier federal regulatory regime may boost investors’ confidence — something industry experts have already caught onto, leading to more optimistic oil and gas M&A forecasts for 2025 and 2026.

Brookfield did not respond to request for comment.

PE portcos also saw some full and partial exits last week, as well as some exits-to-be:

News broke that AlixPartners, a global consulting firm backed by CDPQ, PSP Investment Board, and Investcorp, is preparing to offload a minority stake and has enlisted Goldman Sachs to lead the process. The firm is valued at approximately $8 billion. PSP is expected to sell its stake, though it is unclear whether CDPQ or Investcorp will also participate.

Francisco Partners agreed to sell a significant stake in healthcare software provider Office Ally to New Mountain Capital, valuing the company at $1.8 billion. The partial exit resulted from an auction process and has generated a 9x return for Francisco Partners.

Permira sold its stake in cloud-based HR solutions provider Personal & Informatik AG to Hg for £53 million ($66 million), valuing the company at €5.5 billion ($6 billion). Hg initially invested in the company in 2013, when its enterprise value was approximately €400 million and in 2019 was valued at €2 billion.

MidEuropa sold Regina Maria Group, a private healthcare network, to Mehiläinen, Finland's largest private healthcare provider which is backed by CVC. Financial terms were not disclosed. The is pending anti-trust clearance and is expected to close later this year.

Cinven-backed SYNLAB sold its Spanish clinical diagnostics operations to Eurofins for an unknown sum.

GI Partners completed the sale of Dr. Fortress, a data center service provider, to a consortium comprising FifteenFortySeven Critical Systems Realty and Harrison Street. Financial terms were not disclosed.

Hg sold its stake in smartTrade — a provider of multi-asset trading solutions — to TA Associates for an unknown sum.

Oaktree sold SAF Aerogroup, a French emergency aviation firm, to Infracapital and Vesper Infrastructure at an enterprise value of €300 million.

Meanwhile, portco M&A was in full swing:

KKR-backed Playon, a youth and high school sports content platform, acquired MaxPreps, a high school sports media platform, from Paramount for an unknown sum.

EisnerAmper, a global accounting, tax, and business advisory firm owned by TowerBrook, merged with accounting and consulting firm Prague & Company. Financial terms were not disclosed.

KKR- and TPG-backed A-Gas, a supplier of refrigerants, halon, and other gases used in refrigeration and fire protection industries, bought Refrigerant Services, a Canadian company specializing in the recovery and reclamation of refrigerants. Financial terms were not disclosed.

Doubling down.

I’ve been covering the data center space since early 2022 before ChatGPT launched and the AI revolution began.

Since July 2023, I’ve been reporting that private investors are going to take large losses on these assets. I’ve noted that, despite the potential demand from AI, data centers’ multiples are too high to compensate for the risks incurred by investors: namely, obsolescence risk and climate risk.

When the mega deals came rolling in — Blackstone and AirTrunk, Macquarie and Applied Digital, Brookfield/OTPP and Compass — I did consider changing my tune. Were investors seeing something I wasn’t?

I don’t think so.

Bursting your bubble.

Here are just a few headlines that have solidified my belief that there is a private markets data center bubble ripe for popping:

“China built hundreds of AI data centers to catch the AI boom. Now many stand unused.” by Caiwei Chen (MIT Technology Review): in 2023, following the AI boom sparked by ChatGPT, China experienced a rapid surge in the construction of AI-focused data centers, heavily funded by both government and private investors. Today, up to 80 percent of those new builds are unused due to shifting demand from AI training to real-time AI inference, making many centers obsolete.

“AI excitement didn’t save CoreWeave IPO’s from a lukewarm reception” by Jacob Robbins (Pitchbook News): CoreWeave IPO’ed at $39 per share and closed its first day of trading at $40. The company initially planned to price shares between $47 and $55 (for a $33 billion valuation) but ultimately raised $1.5 billion, selling fewer shares than expected due to concerns about its growing losses, large debt load, and dependency on Microsoft (which accounted for 62 percent of its revenue). CoreWeave’s market cap is $23 billion, similar to its valuation from a secondary transaction in November 2024.

“Microsoft Pulls Back on Data Centers From Chicago to Jakarta” by Brody Ford, Dawn Lim, Olivia Solon, and Faris Mokhtar (Bloomberg): Microsoft has scaled back its global data center expansion plans, halting or delaying projects in regions including the US, UK, Australia, and Indonesia. Analysts suggest the pullback may be due to oversupply in data centers relative to demand. This news comes after reports that Microsoft planned to withdraw from around 2GW of data center projects across the US and Europe.

“Alibaba’s Tsai Warns of ‘Bubble’ in AI Data Center Buildout” by Luz Ding (Bloomberg): “I start to see the beginning of some kind of bubble,” Tsai said at the HSBC Global Investment Summit in Hong Kong. “I start to get worried when people are building data centers on spec. There are a number of people coming up, funds coming out, to raise billions or millions of capital.”

When this bubble pops, the fallout won’t be insignificant. Collectively, private equity has spent an estimated $170 billion on over 450 data center companies since 2022, which is 80 to 90 percent of the total value of deals in this sector for that time period. Blackstone anticipates $2 trillion will be spent on data centers globally by the end of 2029.

I, for one, think the market correction will come much sooner.

See you next week!