M&A Is Risky, But Operating Partners Choose It Anyways

Over half of exits surveyed in Privitas' “Technology: Value Creation 2024” report chose M&A as a path for growth but saw varied results.

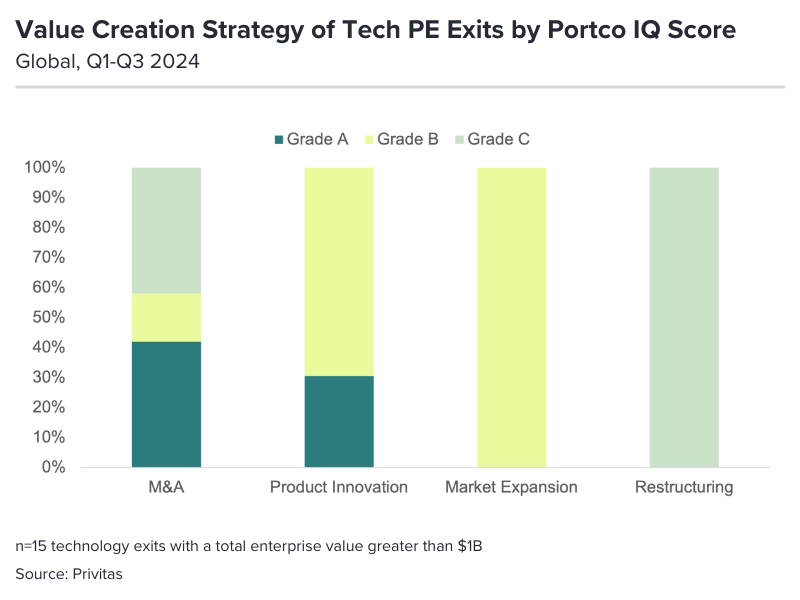

According to a recent study from Privitas, 53% of technology portfolio companies exited between Q1-Q3 2024 used M&A as their predominant strategy for growth and value creation. The outcomes of these exits, however, were varied.

Forty percent of these companies achieved a “Grade A” exit, meaning they were top performers across financial performance, operational efficiency, market positioning, and talent and governance. Meanwhile, 20% achieved a “Grade B” (moderate performers) and another 40% a “Grade C” (underperformers).

On average, surveyed companies using M&A as a value creation strategy exited at a 3.4x enterprise value expansion – the second highest performing result, behind companies who chose market expansion, which garnered a 3.5x EV expansion on average.

And market expansion more consistently delivered returns – according to our report, 100% of companies who chose this strategy for value creation achieved a “Grade A” exit. So why was it the least-used strategy alongside restructuring?

The answer could lie in the fact that PE firms see M&A as a means to market expansion.

“If you're a private equity professional and you want to grow a business, [M&A] is perceived as the easiest to execute approach to get into a new geography, a new product area,” explained Kevin Lehpamer, a partner at law firm Clifford Chance. A large portion of his work focuses on private equity-backed M&A.

He added: “There's probably some perspective that most of the people running private equity funds are deal professionals. So they're very familiar with an execution strategy of doing add-on M&A. You acquire the portfolio company but you want to get into a new geography, product line, or expand the business. You can add on to the existing business in a way that they'll get and can action pretty easily [using M&A].”

And, according to Lehpamer, this has been a trend he has seen throughout his 20-year career.

“M&A being the most common, that is not a blip…I think it's probably the most actionable,” he said. "Other strategies may be perceived to take a little bit more time to develop and play out.”

What might be a blip, however, is how strong M&A has been recently. According to Lehpamer, this is due to higher interest rates.

“If you look at the last decade of private equity, you've seen a lot of roll-up, add-on acquisitions,” he noted. “We've been in a higher interest rate environment and it's harder for funds to raise debt financing. It can be easier to build over time with a series of add on acquisitions where you don't necessarily need large debt financing. If you look at the last few years you will have had more add-ons than if you were to look at the data from, let's say, a dozen or more years ago.”

He added the caveat that M&A tends to be less common in subsectors where there are regulatory barriers to mergers or permitting. However, tech is not one of those industries – indeed, most aren’t.

Cooper Smith, managing director of Privitas and the author of the report, anticipates that this will likely be reflected in the findings of future reports: “40% of PE exits across all sectors in our Portco IQ Index pursued an M&A strategy in 2024. We’re excited to share in future reports how value creation strategies differ by industry, geography, and company size.”